March 5, 2024

Contributed by: Mark Cannella, Extension Associate Professor, University of Vermont

U.S. Crop and Productive Taps

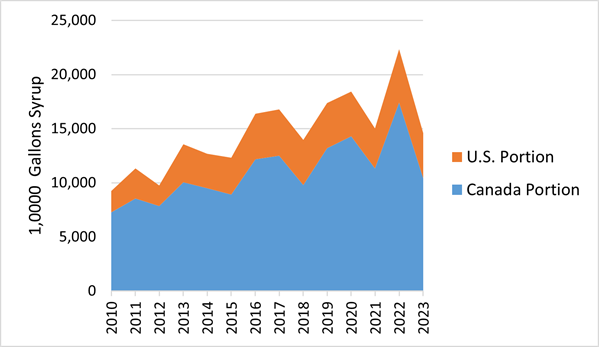

The 2023 U.S. maple syrup crop was down approximately 15% following the large crop in 2022. Regional weather played a major factor in productivity. Production locations on the Southern or “warmer climate” edge of the maple production zone, like certain regions in Ohio, suffered yet another abnormally low production season. Mid-zone regions, like the leading state of Vermont demonstrated very mixed reports based on location and micro-climates. The furthest Northern or “colder climate” edge of the maple production region suffered below average production yields. Maple syrup production declined in all Canadian producing provinces in 2023 compared to 2022. Canada’s leading maple province, Quebec, experienced a 40% decline in reported production in 2023. Figure 1 demonstrates the ongoing yield volatility of this weather sensitive and seasonal crop in the U.S. and Canada.

Figure 1: Combined North American maple syrup production from 2010-2023 (Sources: USDA National Agricultural Statistics Service and Statistique Canada).

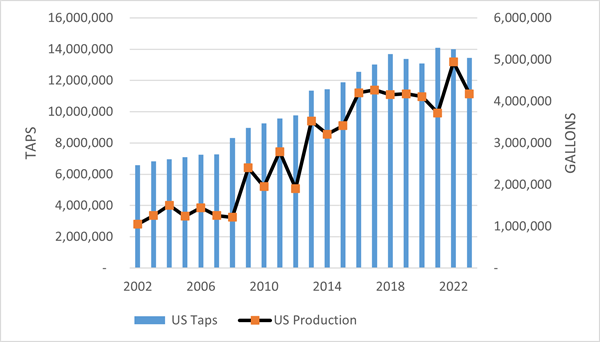

The state of Vermont led all U.S. producing states in 2023 with production of 2,045,000 gallons (23 M pounds) of syrup and 49% of the total domestic crop. New York and Maine are the next most productive states, contributing 18% and 11% respectively to the annual U.S. crop. Total tap count in the U.S. has held relatively level over the past few years at +/- 14 million taps with modest fluctuations up or down. Between 2019 and 2023 the USDA statistical program stopped including information from the states of Ohio, Connecticut, Massachusetts, Minnesota, and Indiana. Those states, while minor in their individual contribution to the U.S. production, reported a cumulative total of approximately 1 million taps in the 2018 report. Using the assumptions that most of those operations are still active, that modest production growth occurred in those states, and the industry-voiced sentiment that this sector is generally underreported in official counts, it is likely that the unofficial U.S. maple tap count could be upwards of 18M taps. Total value of U.S. production is approximately $150M using a three-year average that includes high and low crops totals from 2020-2022.

Canada is the global maple syrup leader and produced an average of 75% of the annual global syrup crop from 2010-2023. Quebec continues to be the most prominent maple province in Canada by producing 90% of their national crop and overseeing well-developed governance programs that exert influence across the industry and markets. The Quebec Maple Syrup Producers (PPAQ) announced the addition of 7 million new maple taps to the member quota beginning in 2024.

In the United States the major producer associations and commercial distributor representatives acknowledge that format statistical undercounting of maple activity and the reported value of production could hinder the industry’s access to services and public programs. The International Maple Syrup Institute (IMSI) is leading a multi-year initiative in partnership with the USDA National Agricultural Statistics Service (NASS) that has already resulted in a revised annual survey to producers. Producers will be continually encouraged to participate in order to improve the official statistics tracking U.S. maple.

Figure 2: United States maple production and total tap count 2002 – 2023 (Source: USDA National Agricultural Statistics Service )

Inputs and Markets

The USD-CAD currency exchange rate continues to hold near $1.35 CAD per $1 USD ($0.74 USD per $1 CAD), the middle of a range established in late 2022. The sustained weakness of the Canadian dollar creates substantial downward pressure on the major U.S. sellers working to compete with syrup imported into the U.S. market. This price pressure carries through with sustained downward pressure on the U.S. producer pay price. The Quebec Maple Syrup Producers (PPAQ) manage the global maple syrup strategic reserve and reported a low inventory of 20M pounds in November 2023. The reserve is projected to drop under 10 M pounds by the start of the 2024 crop year. This is significantly lower than the reserve target level of ~80M -90M pounds or roughly one-half of the annual Quebec maple harvest. Despite low inventories the PPAQ had already established a multi-year pricing agreement (Table 1) with a pre-determined increase to $3.29 CAD$ for the benchmark Golden/Delicate grade syrup. Any supply related price increases for U.S. producers, separate from currency exchange related adjustments on the new $3.29 CAD$, are not expected for syrup purchases from spring to early summer 2024. However, if the 2024 maple harvest is far below average it might prompt U.S. price increases later in 2024.

Table 1: Bulk Maple Prices and Market Factors 2019 to Present

|

|

U.S. Bulk Price1 (Average Across Table Grades) |

PPAQ Golden Price |

USD-CAD Exchange Rate (May to June) |

Inventory Estimates |

|

2019 |

$2.05 - $2.15 USD$ |

$2.94 CAD$ |

1.31 |

Not available |

|

2020 |

$1.95 - $2.00 USD$ |

$2.98 CAD$ |

1.36 |

Average |

|

2021 |

$2.20 - $2.40 USD$ |

$2.99 CAD$ |

1.22 |

Low |

|

2022 |

$2.55 - $2.70 USD$ |

$3.00 CAD$ |

1.27 |

High in U.S. |

|

2023 |

$2.25 - $2.40 USD$ |

$3.20 CAD$ |

1.34 |

Average to High in U.S. |

|

2024 |

Announcement Expected late April-May |

$3.29 CAD$ Amber $3.25 CAD$ Dark $3.18 CAD$ Very Dark $2.84 CAD$ |

1.35 (February 2024) |

Quebec: Low U.S.: No report |

Meanwhile, market sources indicate a softening of growth rates in 2023. The period of Covid-related market growth has ended. An extended period of inflation has increased the cost of living across the U.S. and consumers are becoming more cost conscious with food shopping. While the maple industry has many loyal pure-maple consumers, it becomes more difficult to recruit new users and wholesale buyers to the high quality and high-cost maple sweetener. What’s more, inflation rates have been even higher in Europe and other foreign markets, putting up increased barriers to expanding into other global markets.

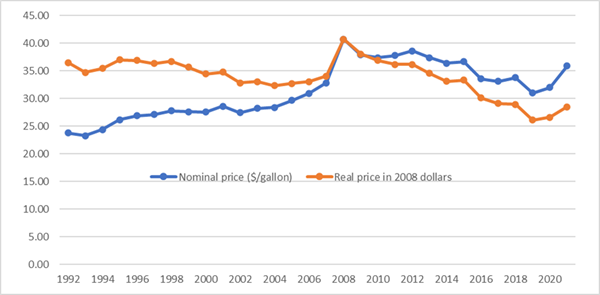

Inflation continues to impact U.S. maple producers with many increased operating costs. The problems for U.S. maple producers are magnified by stagnant prices paid. Figure 3 below shows that when adjusted for inflation, the “real price” received for syrup has been declining over recent years. U.S. maple prices have not increased enough to compensate for inflation and maple producers are forced to operate with less revenue and tighter margins.

Figure 3: Average U.S. nominal and real producer price of maple syrup, 1992 – 2021

Data sources: USDA NASS and U.S. Bureau of Labor Statistics: Consumer Price Index (Credit: Q. Wang, University of Vermont)

Interest rates increased again in 2023 with the Effective Federal Funds Rate (EFFR) topping out at 5.33% in late July. A bright note for 2024 is that efforts to reduce inflation appear to be successful and the Federal Reserve has signaled that rates are likely to drop by around 1% later in 2024. Maple producers with adjustable rate loans have seen debt service payments increase over the past several months. Agricultural lenders indicate the overall increased cost situation is resulting in a slowing of tap expansions by many producers.

Producer Viability Outlook

There continues to be opportunity for managers who are focused on continuous improvement. Utilization of remote vacuum monitoring systems and an emphasis on well-trained employees that can maintain a tight tubing system are key priorities. Achieving 5.5 lbs. -6 lbs. syrup equivalent per tap is realistic for many, and required by some to break-even.

Specialization in sap collection and sales paired with syrup processing partners is gaining more attention in order to right-size investment and improve returns. Sap harvest specialization can reduce start up investment by 30-35% by eliminating the need for syrup processing facilities. Sap buyers can get higher utilization of their existing processing investments to reduce fixed costs. It also enables established brands to increase their supply of syrup and serve a growing customer base. The USDA National Agricultural Statistics service has recently begun tracking sap-only sales to monitor this evolution within the sector.

Weather, Climate and Forest Health Outlook

A wet, cloudy summer in 2023 resulted in reports of anthracnose and other foliar diseases with the potential to produce early leaf drop. Foresters and researchers acknowledge the challenges of measuring short-term impacts on long-lived sugar and red maple tree species. They point out, however, the growing conditions of 2023 are likely to translate to low growth and low stored nonstructural carbohydrates for the 2024 growing season. Forest sites with high water tables and slowly draining soils are likely to have negatively impacted sugar maple root systems as well. Those factors in 2023 could prompt crown dieback in 2024. At the time of this report many maple regions in the U.S. have experienced a mild winter that can increase respiration and increased usage of stored carbohydrates. Maple trees are coming into the production season after a year of less-than-ideal health and growth conditions. It is difficult to predict if these conditions will affect sap flow, sugar content or tree health into summer 2024.

Challenges and Concerns

Climate Questions and Crop Volatility

Producers and buyers are aware of the challenges of crop volatility but it is difficult to separate seasonal weather from climate trends. This is complicated by the high adoption of yield-enhancing technology coupled with the particularities of micro-climates on sap production. Maple specialists who met at the North American Maple Syrup Council 2023 Annual Conference found agreement that adoption of best practices to enhance yields will also be some of the most effective steps to reduce many weather or climate related challenges to yield and tree health. Industry members also see the need to enhance the understanding of their impact on the climate, admitting that the maple community is behind other industries in measuring and evaluating its environmental impact.

Labor

Larger producers continue to voice challenges of finding and retaining labor. A key challenge is securing managerial level employee positions given the unpredictable timing and intense seasonal commitment of the production season. For smaller scale enterprises the timing of family business succession is closely linked to labor management. Senior generation owners must directly address transitions of management and ownership in order to retain willing and able family members to sustain the venture.

Markets

The cost-price squeeze explained in the sections above demonstrates discreet challenges currently experienced across the industry. Strategically, there is lurking uncertainty how the U.S. maple community wants to or can impact longer term trends in the market. There is concern that maple syrup will fall further into the commodity landscape focused on a limited set of pricing features while sacrificing other inherent qualities as a high-quality specialty food. Producers are concerned the U.S. is not doing enough to promote, educate and increase awareness of the many positive features of maple syrup to a broader national audience.

Changes on the Horizon

Industry leaders interviewed for this Outlook want to be better positioned for evolving markets. There is a desire for more consumer-focused research. In order for the industry to remain competitive as a high-priced and high-quality sweetener, sellers seek more information on how to qualify, quantify, communicate and deliver value to consumers. There is interest to explore more innovation in eco-friendly packaging for example. The market focus is expected to focus on Quality Assurance (QA) that satisfies consumers, buyers and regulators. The industry is preparing for increased scrutiny on food safety practices. Members also seek to be prepared to respond to questions about purity, contamination, and environmental impacts.

1 U.S. conventional prices posted in table. Organic premium payments are approximately +$0.15 - +$0.20 per pound.

Editor: Chris Laughton

Contributors: Mark Cannella and Chris Laughton

Mark Cannella is an Associate Professor with the University of Vermont, and he currently directs the UVM Extension Agricultural Business program. Mark is leading a new project from 2023-2026 at the UVM Food Systems Research Center that will begin to measure and monitor the economics and environmental sustainability of the U.S. maple industry.

Mark.Cannella@uvm.edu | 802-881-1576

Farm Credit East Disclaimer: The information provided in this communication/newsletter is not intended to be investment, tax, or legal advice and should not be relied upon by recipients for such purposes. Farm Credit East does not make any representation or warranty regarding the content, and disclaims any responsibility for the information, materials, third-party opinions, and data included in this report. In no event will Farm Credit East be liable for any decision made or actions taken by any person or persons relying on the information contained in this report.

2024 Maple Industry Outlook Webinar

On Wednesday, April 10, Farm Credit East hosted Mark Cannella of the University of Vermont for a look at the Maple syrup and sugar industry in 2024.

- Share this post on